Over $3,000,000 prepayments lost!

By Melvin Yong

By Melvin Yong

December 30, 2021

December 30, 2021

This article is contributed by Melvin Yong, CASE President. Any extracts must be attributed to the author.

Imagine paying thousands of dollars as part of a package to secure a good deal, and the company suddenly goes bust. Surely, the company is obligated to return the money to you right?

Think again.

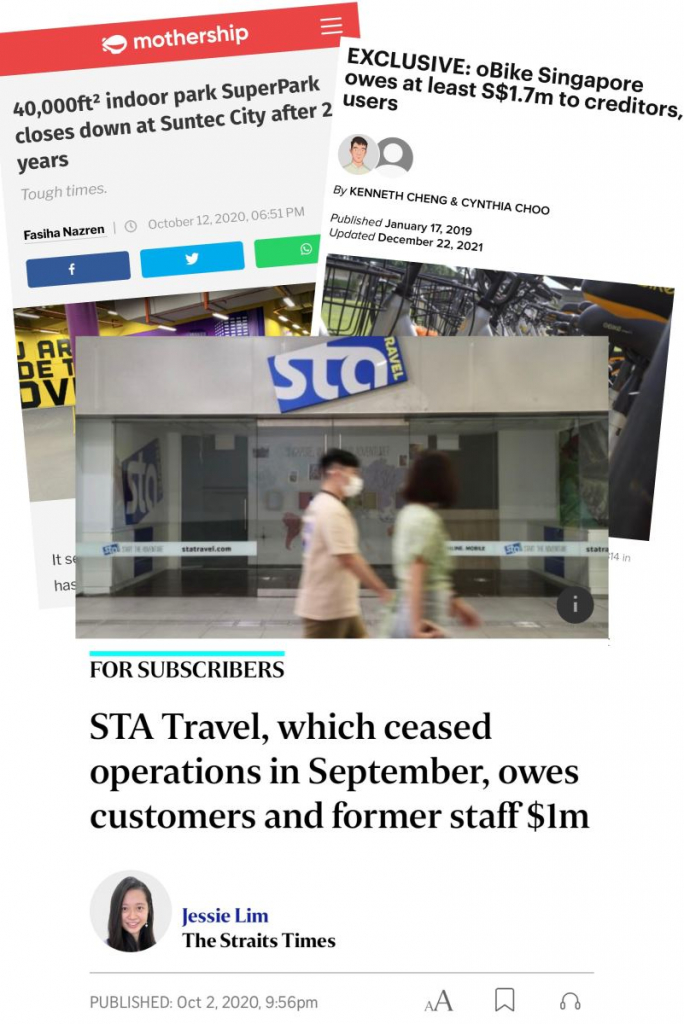

High-Profile Insolvenscies In Singapore

When a company becomes insolvent, our current laws do not sufficiently protect the interests of consumers who might have paid thousands of dollars in prepayments to the company. The administrator assigned to wind up the company will first pay off secured and preferential creditors, such as banks and employees of the company respectively, before dividing whatever remains amongst unsecured creditors, which include customers, suppliers, and landlords.

According to the data from the Consumers Association of Singapore (CASE), consumers reported more than $3 million in prepayment losses since 2019, with several high profile business closures such as STA Travel and SuperPark.

Can We Have Laws To Protect Cosumers Against Prepayment Loses

At this point, you might be wondering – why are there no laws to protect consumers against prepayment losses?

According to the Ministry of Trade and Industry (MTI), prepayments cover a broad spectrum of business activities and it would be overly onerous on businesses if there is a broad-based regulation to govern all aspects of prepayments.

I respectfully disagree.

There is a power imbalance at play, and consumers have the most to lose in the event of sudden business closure.

I hope that the MTI could review industries where consumers report a high amount of prepayment losses, and consider mandating prepayment protection in these industries and/or as part of licensing conditions require the industry to better inform consumers of the steps they can take to protect themselves against business closure.

For instance, since 2015, travel agents are required to seek the decision of consumers regarding the purchase of travel insurance to cover the travel agent’s insolvency.

Working With Trade Associations

To protect consumers’ interests, CASE has been working with trade associations and stakeholders to develop CaseTrust joint accreditation schemes for specific industries that have a high number of complaints. These include the spa and wellness, motoring, and renovation contractors.

Businesses that are CaseTrust accredited are committed to fair business practices and consumer-friendly policies, which include mandatory protection against prepayment and deposit losses[1]. This means that customers would be refunded of their unconsumed but insured prepayments and deposits if the company goes bust.

Since the inception of our prepayment protection requirements in 2011, CaseTrust has protected more than $308 million worth of consumer prepayments.

Today, there are more than 770 CaseTrust accredited entities in more than 10 industries. CASE will step up its efforts to promote CaseTrust accreditation to more industry associations and their members.

Extended Coverage Of Manadatory Cooling-Off Period

Lastly, I think that industries that receive a high number of complaints regarding pressure sales tactics should be subjected to a mandatory cooling-off period, especially if they collect hefty prepayments.

In recent years, the beauty industry received a high number of consumer complaints regarding pressure sales tactics. Many consumers have given us feedback about being aggressively pestered to purchase high priced beauty/massage packages after their free trials or treatments.

Given that such package deals in the beauty industry tend to be big-ticket packages ranging from thousands to tens of thousands of dollars, this is an area of deep concern to CASE.

To minimise the possibility of businesses exerting pressure tactics on consumers as a means of increasing their revenue, I call on the Government to extend the coverage of the mandatory cooling-off period under the Consumer Protection (Fair Trading) (Cancellations of Contracts) Regulations to spa and beauty purchases.

If implemented, a consumer will have the right to cancel a spa/beauty package within a mandatory five-day cooling-off period. This will help reduce the number of pressure sales tactics complaints as consumers will have ample time and space to consider their purchases and not be forced to accept packages sold under pressurising or “compromising” situations.

Conclusion

We often do not expect that a company will close down when we sign package deals or put a lump sum deposit for our purchases. But such cases do happen.

As we ring in 2022, I hope that the Government will review its 2018 position and strongly consider the calls that I have made in this blogpost, so that we can stem the risk of heavy losses that consumers face each year due to prepayment issues.

[1] Businesses accredited under the CaseTrust Renovation and Spa and Wellness schemes are required to protect consumers’ prepayments or deposits.